What we do

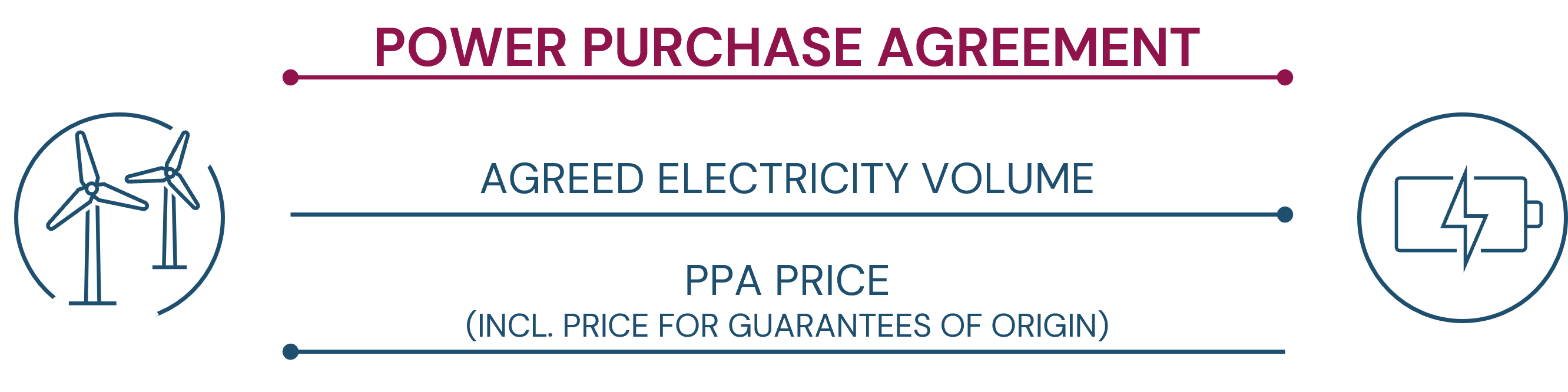

Corporate Power Purchase Agreements (PPAs) are bilateral contracts between a producer of renewable energy and an industrial end user for the supply of green electricity over a long-term period at a price agreed in advance. In principle, PPAs can be divided into physical and virtual/financial PPAs based on the type of electricity delivery. A further division into on-site and off-site PPAs is possible, depending on whether the public power grid is used to deliver electricity or not.

PPAs are procurement contracts that regulate the physical or virtual delivery of renewable energy. They are usually structured as long-term contracts. In addition to the supply of electricity, these contracts also include the delivery of energy attribute certificates (EACs, in Germany: guarantees of origin), which prove the origin of every MWh contracted under the PPA from a specific plant. The price of the certificates is usually included in the total price of the PPA.

From the perspective of an industrial end user, there are usually two main reasons for concluding a PPA.

In principle, there are a variety of classification options for corporate PPAs.

On-site PPAs are characterized by a direct cable connection between the energy-consuming company and the renewable energy plant. The PPA price agreed in an on-site PPA does not include network charges, so on-site PPAs are generally cheaper than off-site PPAs. However, as the system is not connected to the public grid and does not fall within the jurisdiction of the transmission system operator, no guarantees of origin are generally provided to the customer. Although on-site PPAs have long been the dominant form of corporate PPAs, their use is limited due to the lack of suitable locations. Since larger amounts of electricity can usually be purchased as part of off-site PPAs, they have become the dominant type of corporate PPAs.

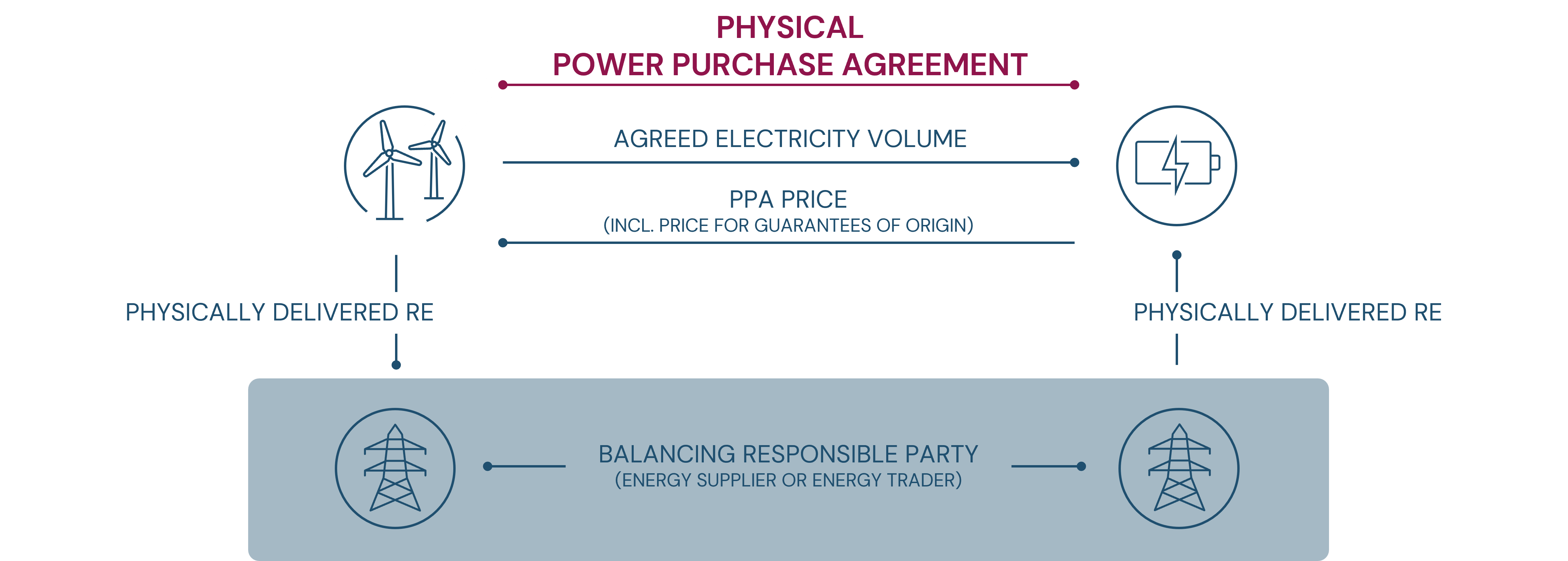

In off-site PPAs, the public power grid is used to transport electricity. As part of the PPA, guarantees of origin are transferred from the Special Purpose Vehicle (SPV) to the industrial end user. This can be done on the basis of two types of off-site PPAs: physical PPAs, which include the physical delivery of electricity from renewable energy sources, and virtual PPAs, which simply provide financial protection against fluctuating electricity market prices.

A physical PPA involves the physical delivery of the contractually agreed amount of renewable energy by a third party (energy supply company or energy trader) via the public power grid. The contract covers the supply of a fixed or variable quantity of green electricity at a bilaterally determined pricing mechanism.

The balancing responsible party (energy supplier or energy trader) receives the green electricity physically from the special purpose vehicle. The industrial end user, in turn, receives the electricity physically from the balancing responsible party. If the balancing responsible party also receives electricity from parties other than the special purpose vehicle (e.g. from fossil power plants), the electricity delivered to the end user may be “grey”.

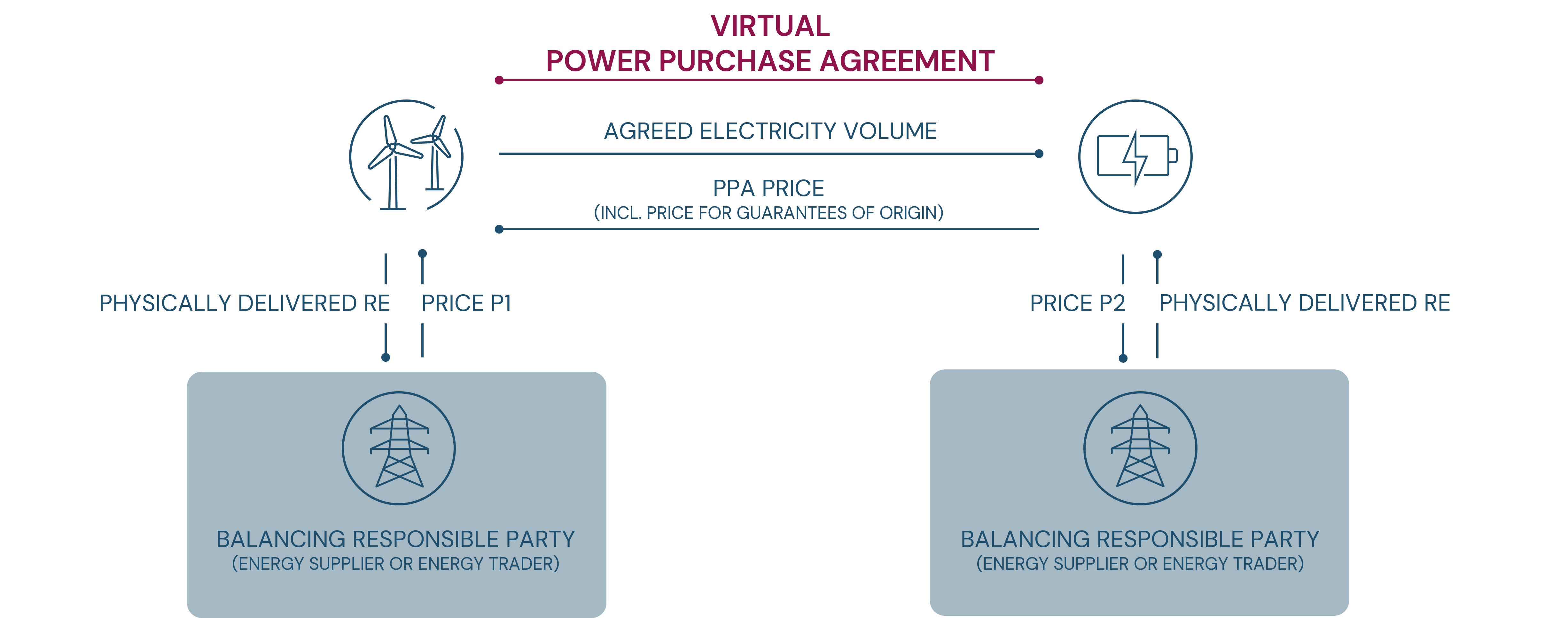

Unlike a physical PPA, a virtual PPA does not involve any physical delivery of electricity between the special purpose vehicle and the industrial end user. It is merely a financial hedge of electricity costs. The PPA price is contractually fixed and there are compensation payments (‘contract for difference’) between the PPA price and the corresponding wholesale electricity price. The physical supply of electricity to the end consumer is carried out by the energy supply company independently of the SPV's electricity production. Green electricity certificates (guarantees of origin) can also be transferred in virtual PPAs, enabling the industrial end user to achieve a decarbonisation effect.

In a Contract for Difference (CfD), the current market price on the day-ahead market (settlement price) is used as the basis for the virtual PPA. In addition to setting the settlement price, both parties agree on a so-called strike price, which serves as a benchmark and is fixed for a specific period of time (duration of the PPA). There are three possible scenarios for price development:

Scenario 1: Settlement Price (Market Price) > Strike Price

In this case, the special purpose vehicle would earn more than agreed because it had agreed with the end user on a strike price (fixed price) lower than the market price. In order to stick to the agreed price, the special purpose vehicle must compensate the industrial end user by paying the difference between the settlement price and the strike price to the end user.

Scenario 2: Settlement price (market price) < Strike Price

In this case, the end user would consume electricity at a lower cost than agreed under the virtual PPA. The special purpose vehicle would earn less than it is entitled to under this contract. As a result, the end user must pay the difference between the fixed strike price and the settlement price to the special purpose vehicle.

Scenario 3: Settlement Price = Strike Price

In this case, no one has to compensate the respective opposing party.

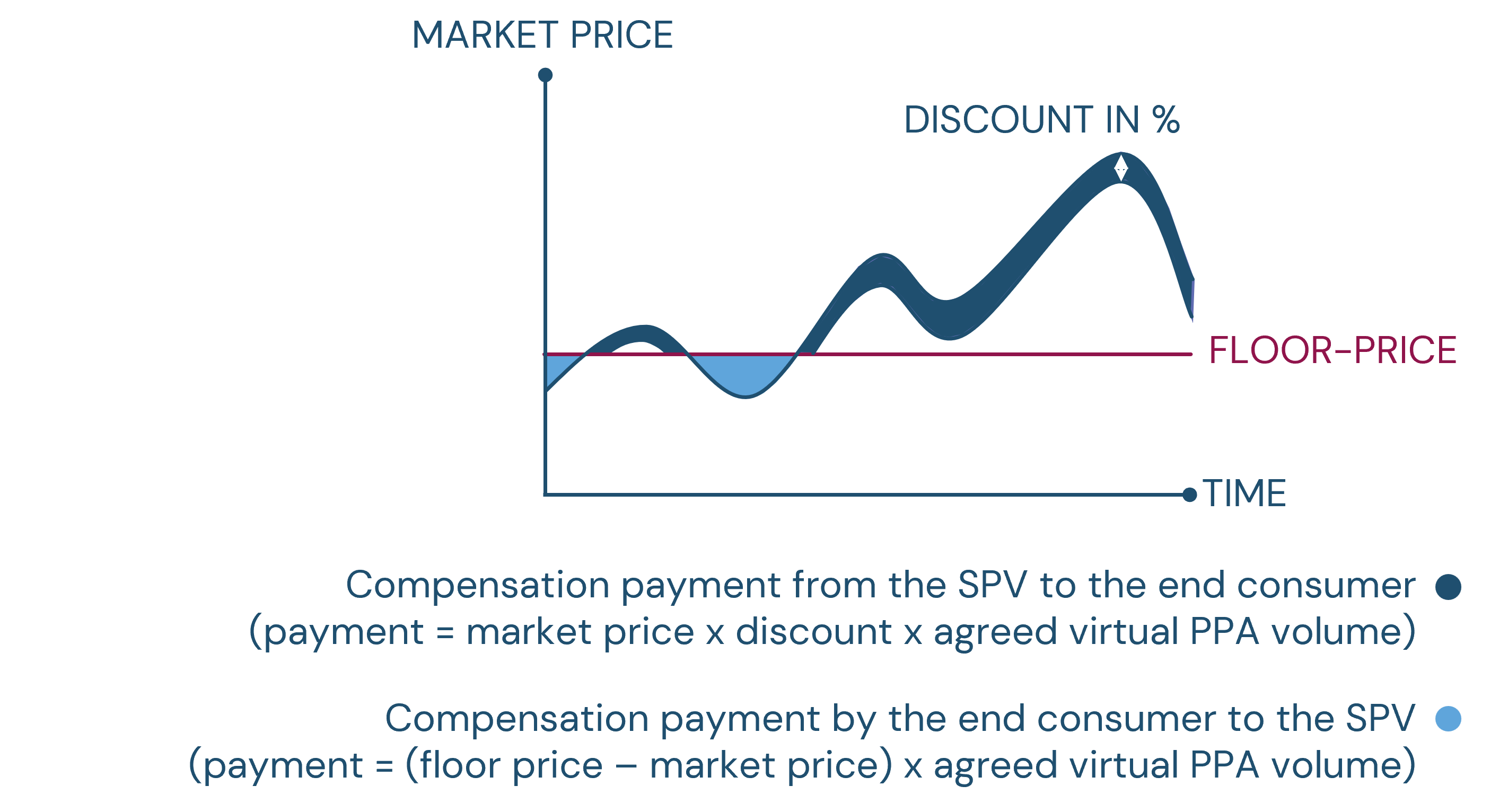

A Contract for Difference (CfD) /Fixed for Floating PPA offers the highest level of revenue security from the point of view of the special purpose vehicle and is therefore the most attractive option from a lender's point of view. The strike price is usually higher than the floor price in a market following PPA.

Market Following PPAs increase the opportunity for the seller to benefit from rising market prices while reducing the payment risk for the end consumer. However, the floor price is usually lower than the strike price agreed in the CfD, which means a lower income security from the point of view of the SPV lender.

There are three possible scenarios for price development:

Scenario 1: Settlement price (market price) > floor price

In this case, the special purpose vehicle would earn more than agreed because it had agreed with the end user on a lower floor price compared to the market price. The special purpose vehicle must therefore compensate the industrial end user by making a compensation payment in the form of a discount at the market price.

Scenario 2: Settlement price (market price) < floor price

In this case, the end user would consume electricity at a lower cost than agreed under the virtual PPA. The special purpose vehicle would earn less than it is entitled to under this contract at least. As a result, the end user must pay the difference between the fixed floor price and the settlement price to the special purpose vehicle.

Scenario 3: Billing price = floor price

In this case, no one has to compensate the respective opposing party.

It should be noted that other pricing mechanisms such as a cap or collar may also be used as part of corporate PPAs.

How many guarantees of origin are delivered as part of a PPA depends on the agreed volume structure, i.e. on whether the end user receives a fixed volume of electricity (so-called fixed volume PPA) or a variable quantity (so-called as produced PPA). In the case of a fixed volume PPA, the number of guarantees of origin delivered corresponds exactly to the fixed amount of electricity agreed in advance. If the renewable energy plant produces a lower amount of electricity than was contractually agreed, the special purpose vehicle is obliged to buy the residual amount of electricity and guarantees of origin on the secondary market and deliver it to the end user.

From the end user's perspective, a fixed volume PPA is the preferred volume structure in most cases, as predictable quantities are delivered and these can be better tailored to their own electricity consumption.

In contrast to fixed volume PPAs, Pay as Produced PPAs deliver exactly the amount of guarantees of origin that corresponds to the amount of electricity generated by the renewable energy plant. In a Pay as Produced PPA, end consumers bear the risk that the special purpose vehicle does not deliver the expected electricity production. In the event of underproduction, the end user must buy the missing amount of electricity and the corresponding guarantees of origin at market prices on the intraday electricity market.