What we do

EEG 2027 is not a political option or voluntary reform, but is required within the framework of state aid approval and EU Climate State Aid guidelines. As a result of the temporary state aid approval of the existing EEG, Germany must adapt its funding mechanisms to current EU requirements by 2027 at the latest. The introduction of a reformed EEG 2027 is therefore necessary as part of the current reform discussion and not just a question of political design. Against this background, the German energy industry is facing significant structural change.

The reformed Renewable Energy Act (EEG 2027) expected in 2027 marks a structural realignment of funding mechanisms for wind energy, photovoltaics and other renewable power generation technologies. For project developers, investors, energy suppliers and companies in the area of Power Purchase Agreements (PPAs), this creates new opportunities, but also changes in the framework for financing and marketing.

One of the key developments in the EEG 2027 is the stronger focus on the electricity market. The previous system of fixed or highly predictable feed-in tariffs is increasingly being replaced by funding mechanisms closer to the market. The focus is in particular on difference-based remuneration systems that are based on the actual market price for electricity.

This model is often discussed as a development towards so-called Contracts for Difference (CfD). The aim is to make the promotion of renewable energy more efficient and at the same time to integrate it more closely into the electricity market. For operators of wind farms and photovoltaic systems, this means a significantly closer link to price developments on the electricity exchange.

The structure of EEG tenders will also be further developed as part of the reform. In the future, systemic criteria will be increasingly taken into account in addition to the pure price offer. These include network and system serviceability, integration into the power grid and potential contributions to supply security and system stability.

This adjustment of tender designs leads to greater differentiation between projects. While it was primarily the cheapest price that was decisive so far, qualitative criteria will gain in importance in the future. For wind energy and photovoltaic project developers in Germany, this means a strategic realignment of the bidding and project structure.

Contrary to frequent discussions, the current draft EEG 2027 does not provide for a direct reduction in the maximum bid values in tenders. The maximum values remain an administrative instrument of the Federal Network Agency and are determined primarily on the basis of past surcharge values and market developments.

This does not result in a political definition of a new price cap, but an indirect adjustment via market mechanisms. However, falling project costs or intensive competition in the renewable energy sector can also result in a reduction in the achievable bid values over the long term.

Another important aspect of the EEG reform concerns the flexibilization of funding and participation options. As part of the planned realignment, it is being discussed how to reduce or standardize existing opt-out options. The aim is to create a clearer and more uniform market structure for new renewable energy plants.

For operators, this means greater standardization of participation conditions in future EEG tenders.

Protection of existing wind energy and photovoltaic plants is essential for investors and operators of existing wind energy and photovoltaic plants. Systems that have already received an EEG tarif or went into operation before the new regulations came into force generally remain in the existing funding system.

This means that funding conditions once granted will continue to apply and will not be amended retroactively by the EEG 2027. This planning security remains a central pillar of the energy transition in Germany and is particularly important for financing renewable energy projects.

The EEG 2027 provides new impetus for the market for power purchase agreements (PPAs) and direct marketing. Greater market integration and the possible approximation to CFD-like structures increase the importance of long-term power purchase agreements.

Companies that procure renewable electricity via PPAs must prepare for more volatile market prices, but at the same time benefit from a growing range of directly marketed green electricity volumes from wind and solar projects.

The EEG 2027 does not mark a radical break, but rather a development towards a more market-oriented promotion of renewable energies. While the basic principles of the energy transition remain in place, the focus is shifting significantly towards market integration, system efficiency and competitive tenders.

For project developers, investors and companies in the renewable energy and PPAs sector, this means increased complexity, but also new strategic opportunities. In particular, the combination of market price dynamics, tender competition and direct marketing will play an even more central role in the future.

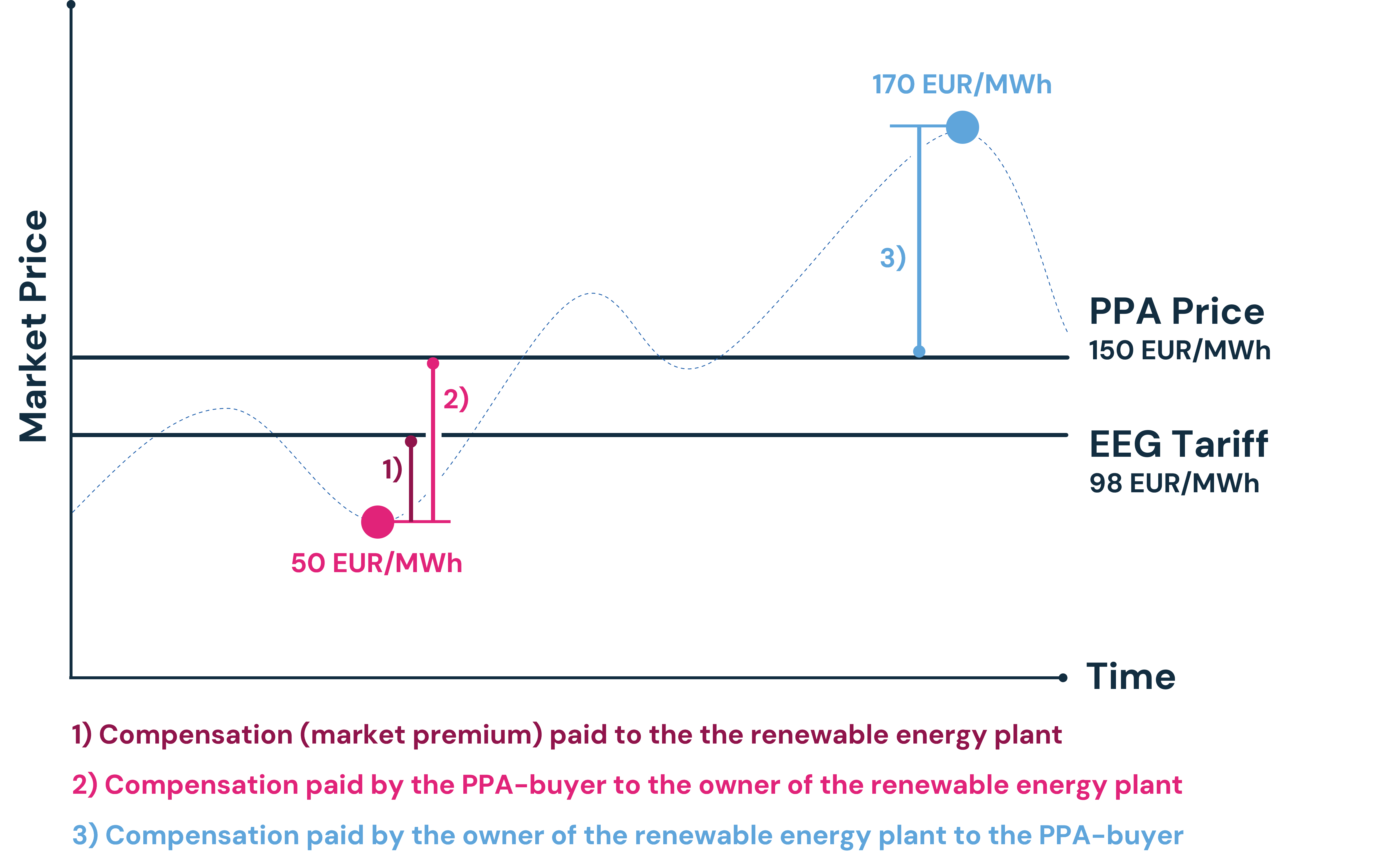

In the existing EEG world (up to 31.12.2026), an applicable value of 70 EUR/MWh is assumed for onshore wind, which rises to 98 EUR/MWh taking into account a correction factor of 1.4. Marketing is carried out via direct marketing in the EEG system, where the reference market value is not to be understood as a simple average price, but as a technology-specific, production-weighted monthly market value based on spot market prices. Two scenarios are assumed for the analysis: a high-price scenario with a reference market value of 170 EUR/MWh and a low-price scenario with a reference market value of 50 EUR/MWh. In addition, in both cases, a virtual PPA (VPPA) with an industrial company with a strike price of 150 EUR/MWh and a term of one year is assumed.

In a high-price scenario (reference market value 170 EUR/MWh), the reference market value is above the applicable value of 98 EUR/MWh, meaning that there is no market premium. The operator therefore only achieves the market value of 170 EUR/MWh from direct marketing. In addition, the VPPA results in a compensation payment to the offtaker of 20 EUR/MWh (170EUR/MWh market price minus 150 EUR/MWh strike price). This results in total revenue of 150 EUR/MWh.

In a low price scenario (reference market value 50 EUR/MWh), the reference market value is below the applicable value, resulting in a positive market premium of 48 EUR/MWh (98 EUR/MWh minus 50 EUR/MWh). The operator therefore receives 50 EUR/MWh from direct marketing plus 48 EUR/MWh market premium, which corresponds to EEG revenue of 98 EUR/MWh. In addition, the VPPA results in compensation of 100 EUR/MWh (150 EUR/MWh strike price minus 50 EUR/MWh market value). This results in total revenue of 198 EUR/MWh.

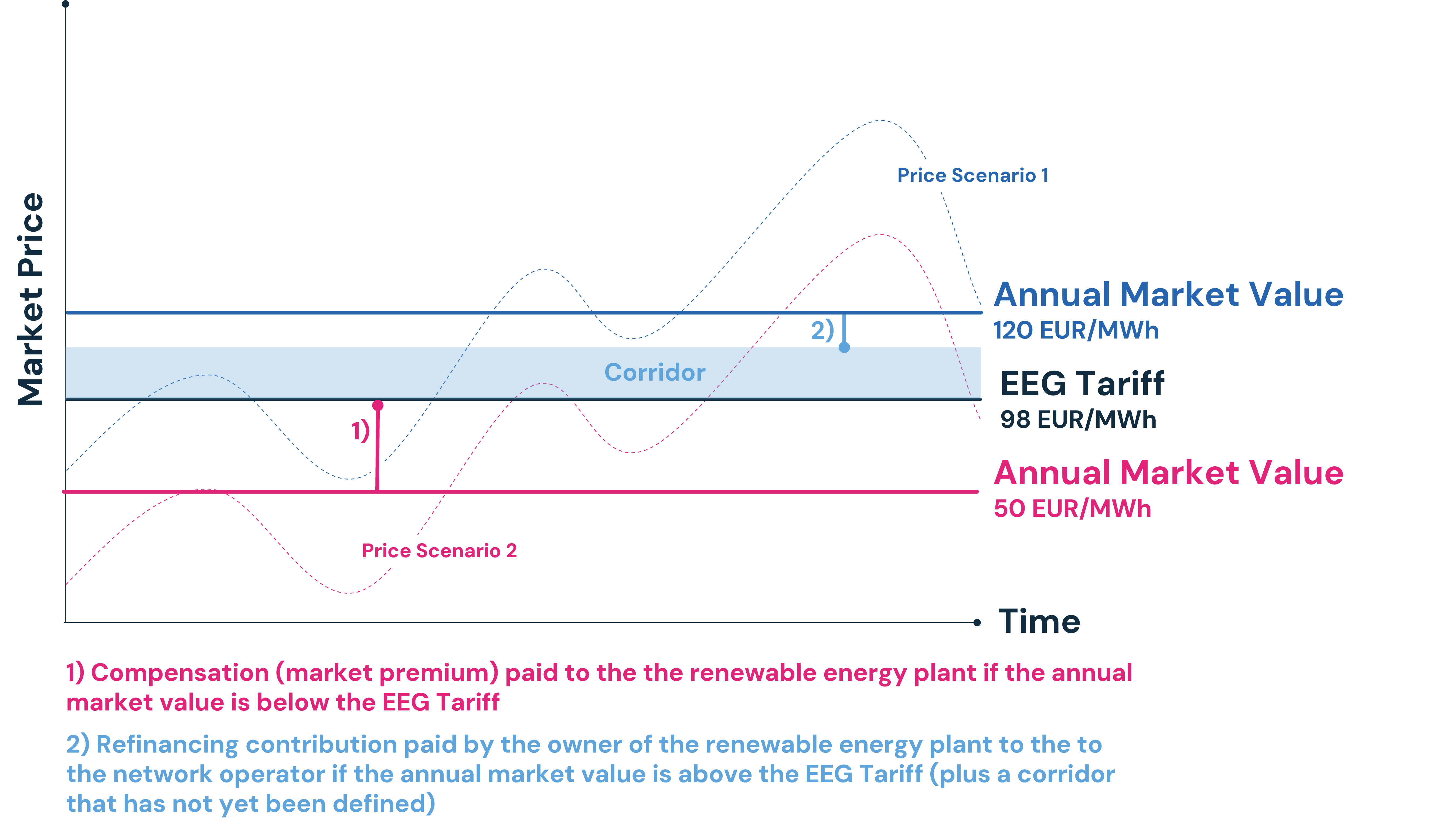

Following the key points of the 2027 EEG reform currently discussed, the funding regime for new investments in the renewable energy sector is being further developed towards a two-sided contract-for-difference (CfD) -like system. The value to be applied continues to serve as a central reference value and corresponds economically to the guaranteed target revenue per megawatt hour generated. In contrast to the previous market premium logic, however, there is a complete symmetrical settlement between market price and applicable value: If the annual market value is below the value to be applied, the operator receives a compensation payment; if, on the other hand, the annual market value exceeds the applicable value (plus a corridor to be defined), a refinancing contribution is returned to the network operator.

It is therefore currently envisaged that the funding mechanism will be explicitly designed as a two-sided (CFD-like structure) difference agreement. At the same time, according to the current state of discussion, the system of location differentiation will probably not be completely abolished, but will be integrated into the definition of the applicable value or more endogenized in the tender design. A separate, isolated correction factor in the previous form (multiplier logic) could be omitted or converted into a finer location-dependent bid evaluation in order to continue to reflect the economic efficiency of different wind sites, but to integrate them more systemically into pricing.

The case study assumes an applicable value of 98 EUR/MWh and considers two market scenarios: a high-price scenario with an annual market value of 120 EUR/MWh and a low-price scenario with an annual market value of 50 EUR/MWh.

In a high-price scenario (120 EUR/MWh), the annual market value exceeds the applicable value, meaning that the difference of 22 EUR/MWh is attributable by the operator to the EEG system (this value may be reduced by introducing the corridor). The net revenue is thus leveled to the fixed target value of 98 EUR/MWh. An additional virtual power purchase agreement (VPPA) can no longer be combined as an “on-top structure” as part of the EEG CFD system, as the funding logic already ensures complete price smoothing at project level. Either participation in the CFD system or complete market marketing takes place outside the EEG regime.

In a low price scenario (50 EUR/MWh), the compensation mechanism works in the opposite direction: The operator receives a funding payment of 48 EUR/MWh, so that the total revenue is again raised to 98 EUR/MWh. Here, too, an additional VPPA structure within the EEG system is not provided. Outside the EEG CFD regime, a VPPA could generate financial compensation of 100 EUR/MWh (150 EUR/MWh strike minus 50 EUR/MWh market price) at the same market price, but would require a complete decision for a market marketing model. As a result, the EEG 2027, as modeled here, leads to a clear system separation between state-backed CFD revenue and fully market-based PPA/VPPA structures without combinable “stacking” effects.

In the event of a complete exit from the EEG CFD system and a purely market marketing of electricity generation, the operator can realize the revenues exclusively via the spot market in combination with a virtual power purchase agreement (VPPA). It is assumed that the spot market price corresponds to the respective reference market value and that the VPPA is designed as a financial difference contract with a strike price of 150 EUR/MWh. In a high-price scenario with a market price of 170 EUR/MWh, the operator initially generates physical market revenue of 170 EUR/MWh. In addition, the VPPA results in a compensation payment of 20 EUR/MWh (difference between strike and market price), which is to be paid to the offtaker, resulting in total revenue of 150 EUR/MWh. In a low price scenario with a market price of 50 EUR/MWh, the market revenue accordingly remains at 50 EUR/MWh, while the VPPA generates a significantly higher compensation of 100 EUR/MWh. In this case too, this results in total revenue of 150 EUR/MWh. Overall, in both market scenarios, the VPPA results in a complete price smoothing to the agreed strike price, as a result of which the operator realizes a stable, contractually fixed revenue stream of 150 EUR/MWh regardless of the market price level.