What we do

Virtual Power Purchase Agreements (VPPAs) are becoming massively important in business practice, as they represent a highly flexible alternative to physical supply contracts. Their key advantage is that they can be completed largely independently of balancing group managers and the physical network infrastructure, while still offering all the strategic advantages of a physical PPA. Through VPPAs, companies benefit from asset-specific contracting, which enables a direct connection to specific renewable energy investments, and secure the appropriate asset-specific guarantees of origin (GOOs) for their sustainability goals. At the same time, they act as an effective instrument for price hedging against fluctuating electricity prices on the spot market by creating a long-term calculation basis.

For a detailed explanation of how virtual PPAs work, click here.

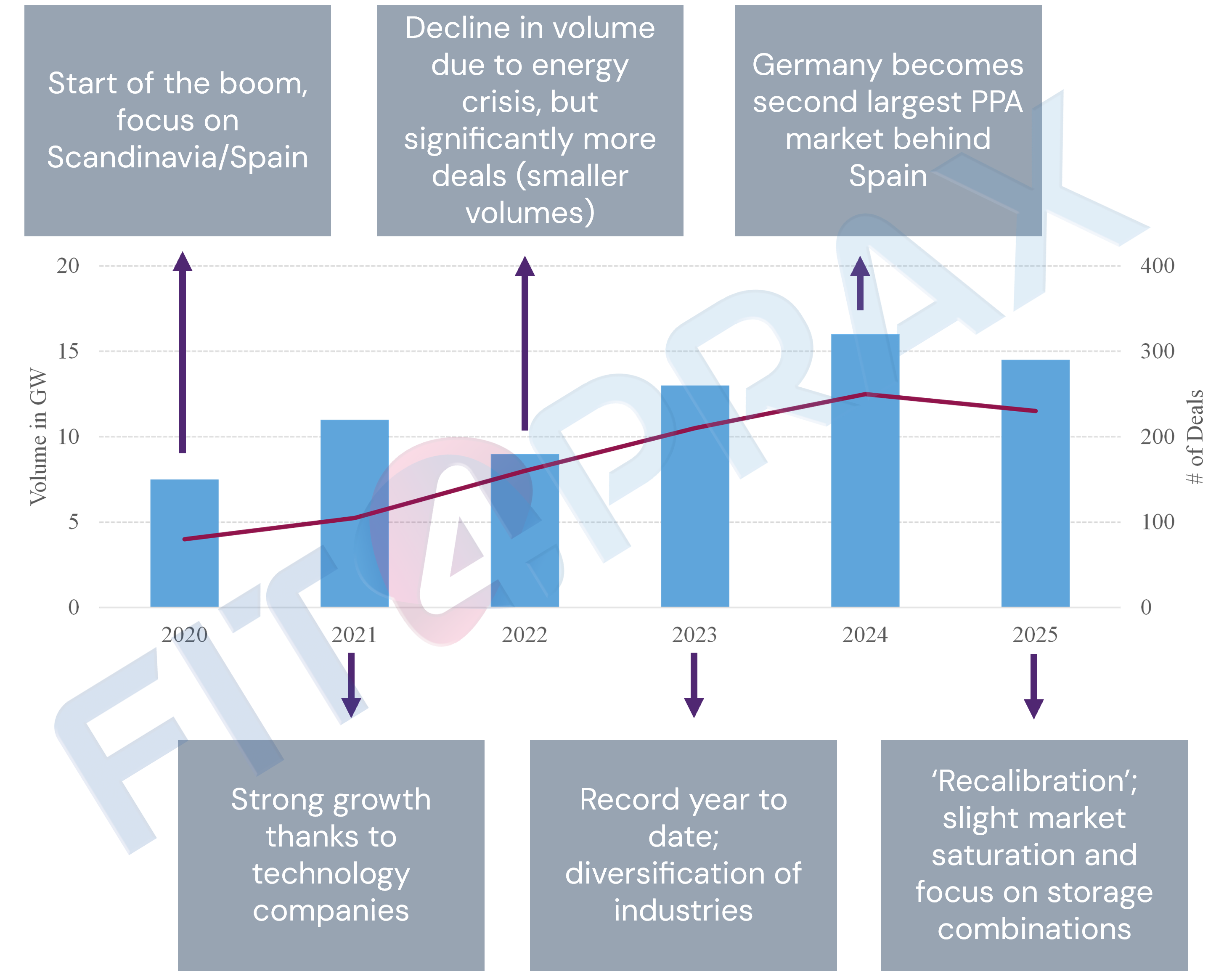

In the last five years, the market for (v)PPAs has changed from a niche market for tech giants to a central risk management tool for the broad industry. This development took place in several phases: Between 2020 and 2021, VPPAs were primarily used for “green marketing” and the achievement of sustainability goals by global corporations. Volumes were concentrated in a few pioneering markets, such as Spain and Scandinavia. In 2022, the energy crisis acted as a catalyst. The focus suddenly shifted from ecology to economic security. VPPAs became indispensable as a “hedge” against exploding spot market prices. In the following years 2023 to 2025, the European VPPA market achieved record volumes and a new geographical breadth, with Germany becoming the top market. VPPAs are now standardized and accessible to SMEs. However, the accounting presentation of this type of contract remains one of the biggest hurdles why institutional end users are reluctant to conclude these contracts.

From a balance sheet perspective, VPPAs are generally classified as financial instruments under IFRS 9. Since a virtual PPA does not involve a physical flow of electricity between producer and consumer, but only price differences between the agreed strike price and the market price (sell and buy side) are financially balanced (Contract for Difference), they have a clear derivative character. However, as these instruments do not bear interest and therefore do not meet the strict criteria of the Solely Payments of Principal and Interest (SPPI) test, an evaluation of amortized costs is excluded. As a result, VPPAs must be rated at Fair Value through Profit or Loss (FVTPL) by default. This means that, as part of the mark-to-market valuation, they are recognized at fair value in the balance sheet, with changes in value directly affecting the result for the period.

Since a virtual PPA is classified as a non-derivative financial instrument, the balance sheet is initially recorded in accordance with the Fair Value through Profit or Loss (FVTPL) measurement standard. In practice, this means that the VPPA must be constantly reassessed within each settlement period when market expectations change. Since the fair value depends significantly on the development of future electricity market prices, any adjustment to the forward curve results in immediate and often significant profit and loss recognition in the profit and loss statement (P&L). Without corrective measures, this would create artificial volatility in net income, which distorts the company's actual economic performance, even though the cash flow effects are only well into the future.

In order to neutralize these unwanted earnings fluctuations, the VPPA can be designated as a hedging instrument as part of hedge accounting. For this to be admissible, the company must prove that there is a highly likely underlying transaction, which is covered by the VPPA. In the case of an end user, this basic transaction is the continuous purchase of physical electricity at variable market prices. Since changes in the market price of physical purchases directly influence the company's cash flows, the VPPA acts as an economic counterbalance: The risk of fluctuating payouts for electricity consumption is offset by the opposing compensation payments from the VPPA derivative.

As soon as the VPPA has been formally designated as a cash flow hedge, the changes in the market value of the derivative are no longer recorded directly in the income statement, but are initially posted in equity through other earnings (OCI). A reclassification from the OCI into the P&L only takes place at the time when the underlying underlying transaction — i.e. the actual electricity consumption — also has an impact on earnings. This so-called “recycling” mechanism combines the expenses for the physical purchase of electricity and the income or expenses from the VPPA in the same period. This smooths out the balance sheet and correctly reflects the economic reality of price hedging, as the company is presented on the balance sheet as if it had contracted a fixed electricity price.

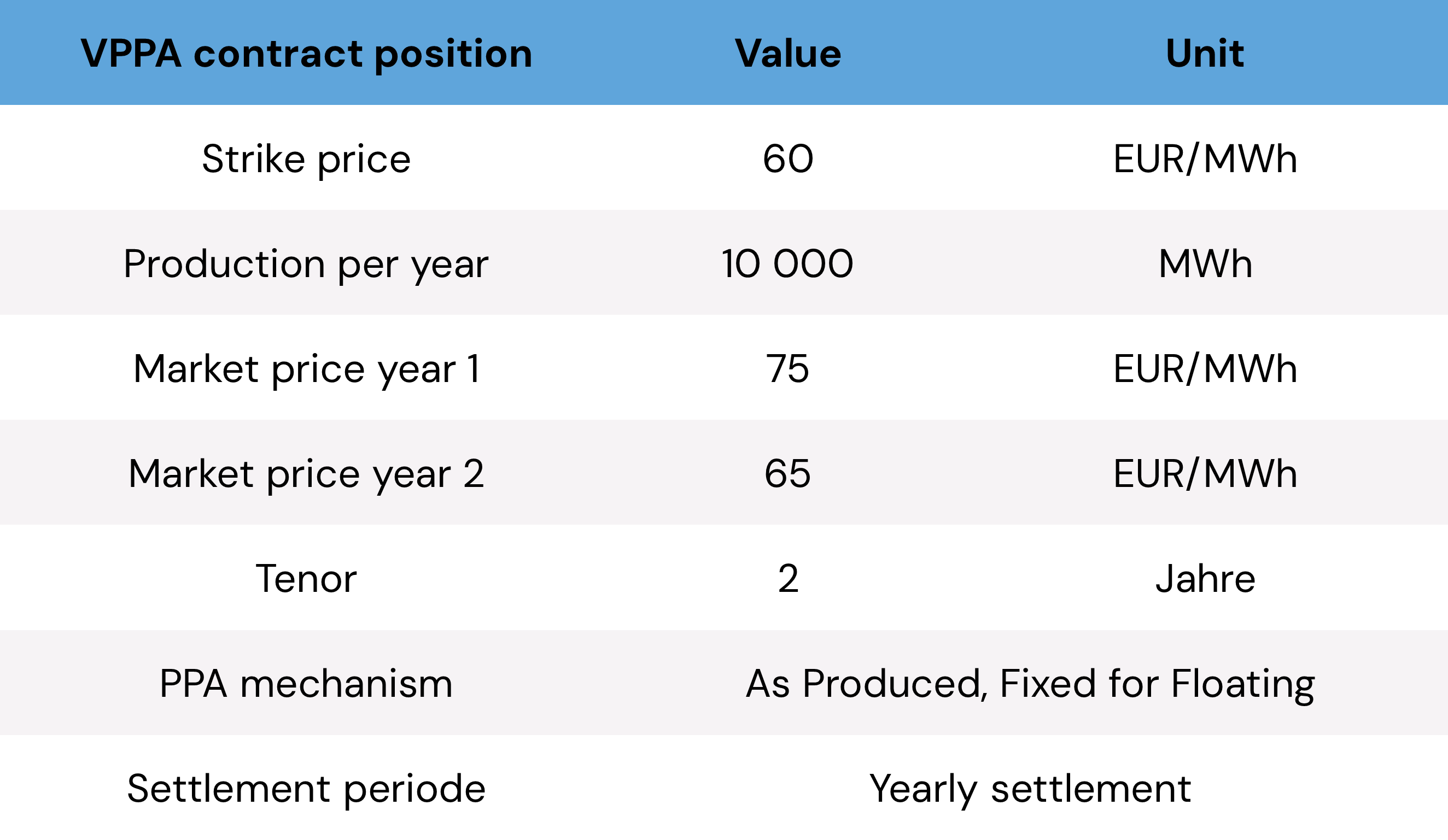

The accounting treatment of the VPPA for one year within the term is presented below, assuming that it is designated for hedge accounting. The hedging volume is assumed to be below physical power consumption, so that there is no ineffective part of the hedge (which would have to be immediately recognized at fair value in profit). The following table shows the main PPA assumptions.

A discount rate of 5% over the two years can also be assumed. This results in a cash flow of (75-60) x 10,000 = 150,000 EUR in year 1 and (65-60) x 10,000 = 50,000 EUR in year 2. The fair value evaluation results in the following values:

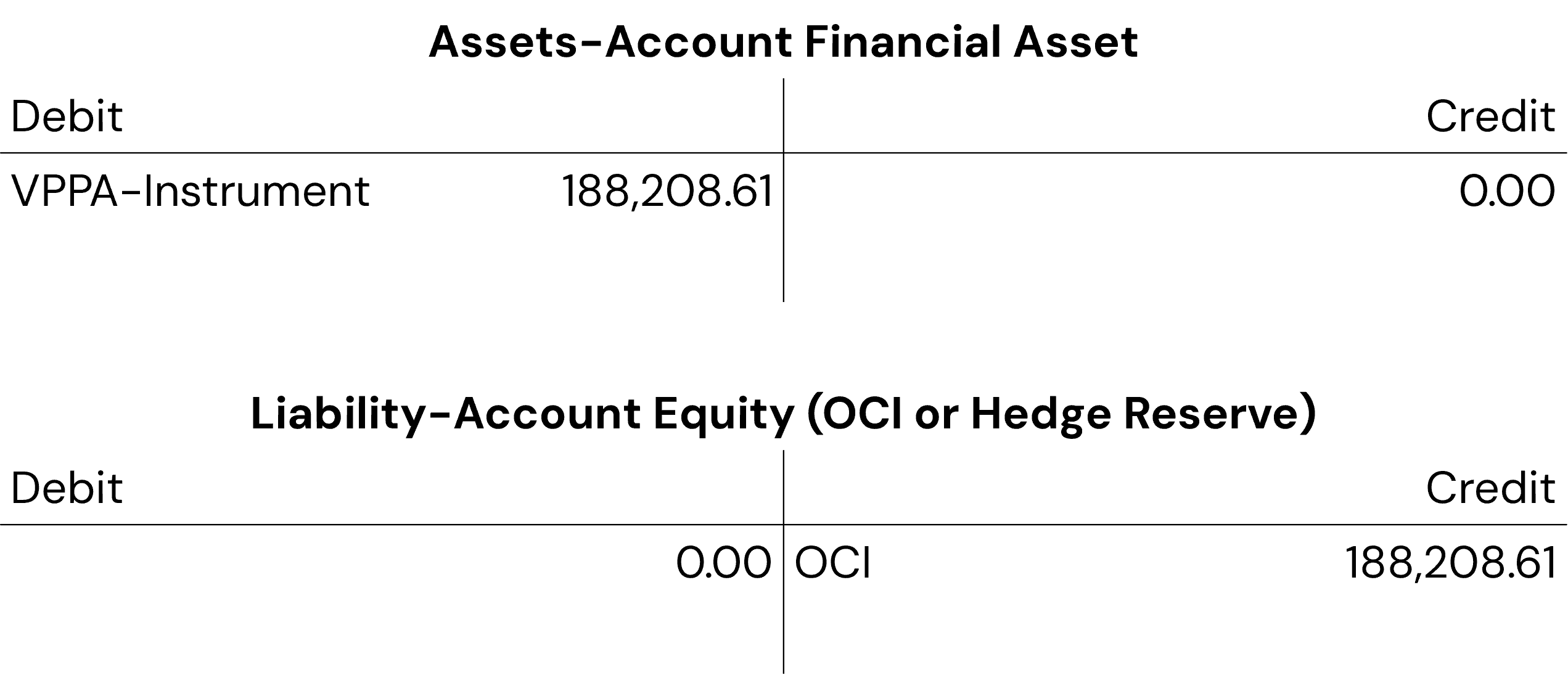

The balance sheet effect of hedge accounting for the initial and subsequent valuation is set out below.

1. Evaluation at the time of VPPA conclusion (initial evaluation)

2.1 Assessment in year 1

Note: The difference between the present value a year ago and today's payment is the interest effect over time.

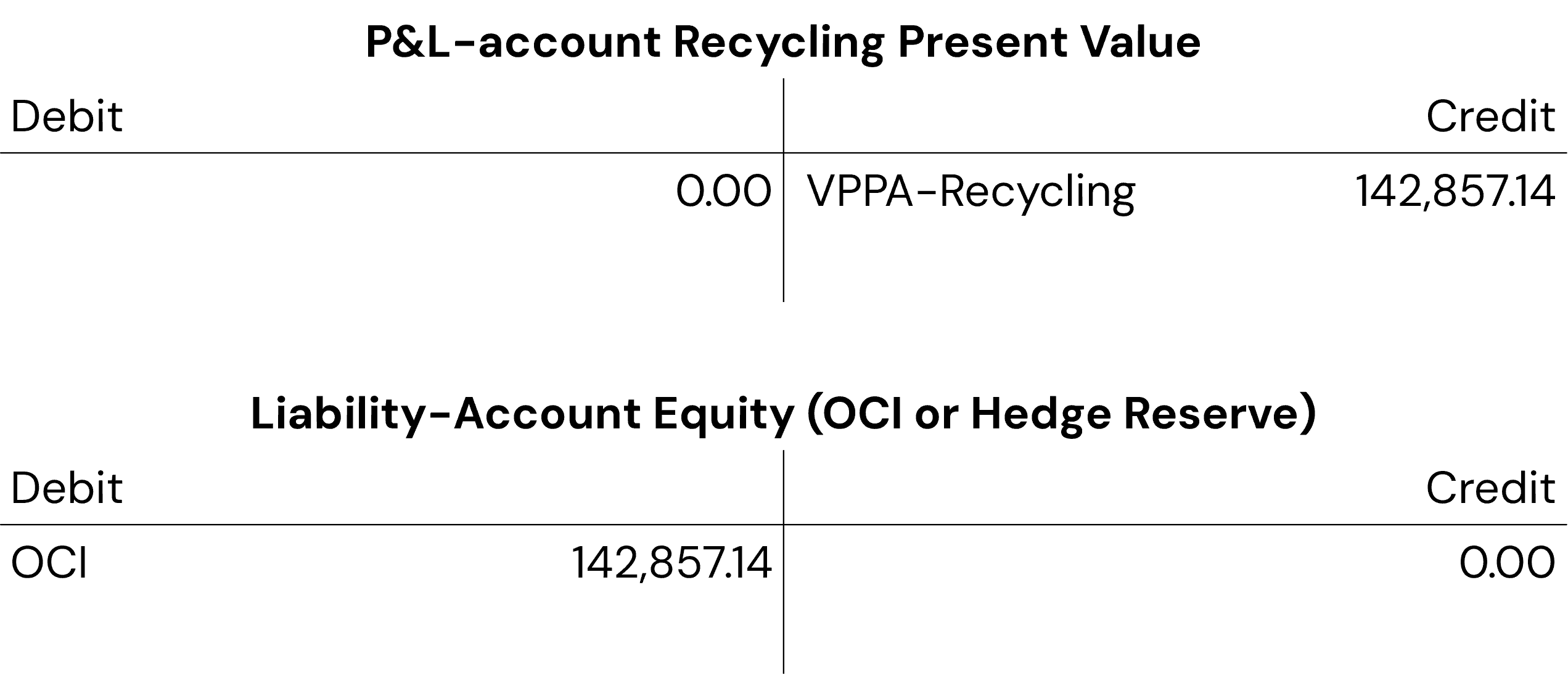

2.2 Recycling in year 1

Note: In year 1, 142,857.14 EUR will be recycled from the initial valuation at the end of the first year. As a result of the compound interest effect, the final value is 150,000 EUR, which in the present case flows to the electricity consumer/offtaker from the VPPA in cash. For this reason, the company posted an additional income of 7,142.86 EUR in year 1. This compound interest-related income is also known as “unwinding.”